NFT Lending: A New Hybrid Mechanism Joins The Space

NFT Lending: A New Hybrid Mechanism Joins The Space

The ins and outs of NFT financialization

If you have not looked into the NFT financialization space and want to get yourself familiarized with the current market landscape, you can refer back to my previous research. The piece explained the importance of NFT financialization, as well as the bottlenecks, market landscape, and potential opportunities in the space.

Today I am diving into NFT lending, where we have already seen lots of protocols try to solve the NFT liquidity issue and release potential liquidity locked within NFTs.

What is NFT collateralized lending?

NFT collateralized lending works in the same way as that of lending in traditional finance, in which the creditor provides liquidity to the debtor. The difference between NFT lending and traditional finance lending is the collateralized asset. Traditional finance leverages assets such as real estate, stocks, equipment, land etc. as collateral, while NFT lending protocols use NFTs as collateral and the value of NFTs to determine the loan amount, interest rate and loan duration.

Builders in the NFT space have developed and are continuing to develop various mechanisms that make NFT collateralized lending a reality. Let’s take a moment to refresh our collective memory about the existing NFT lending mechanisms that protocols have developed which enable NFT-as-collateral loans.

Existing mechanisms and analysis of pros and cons:

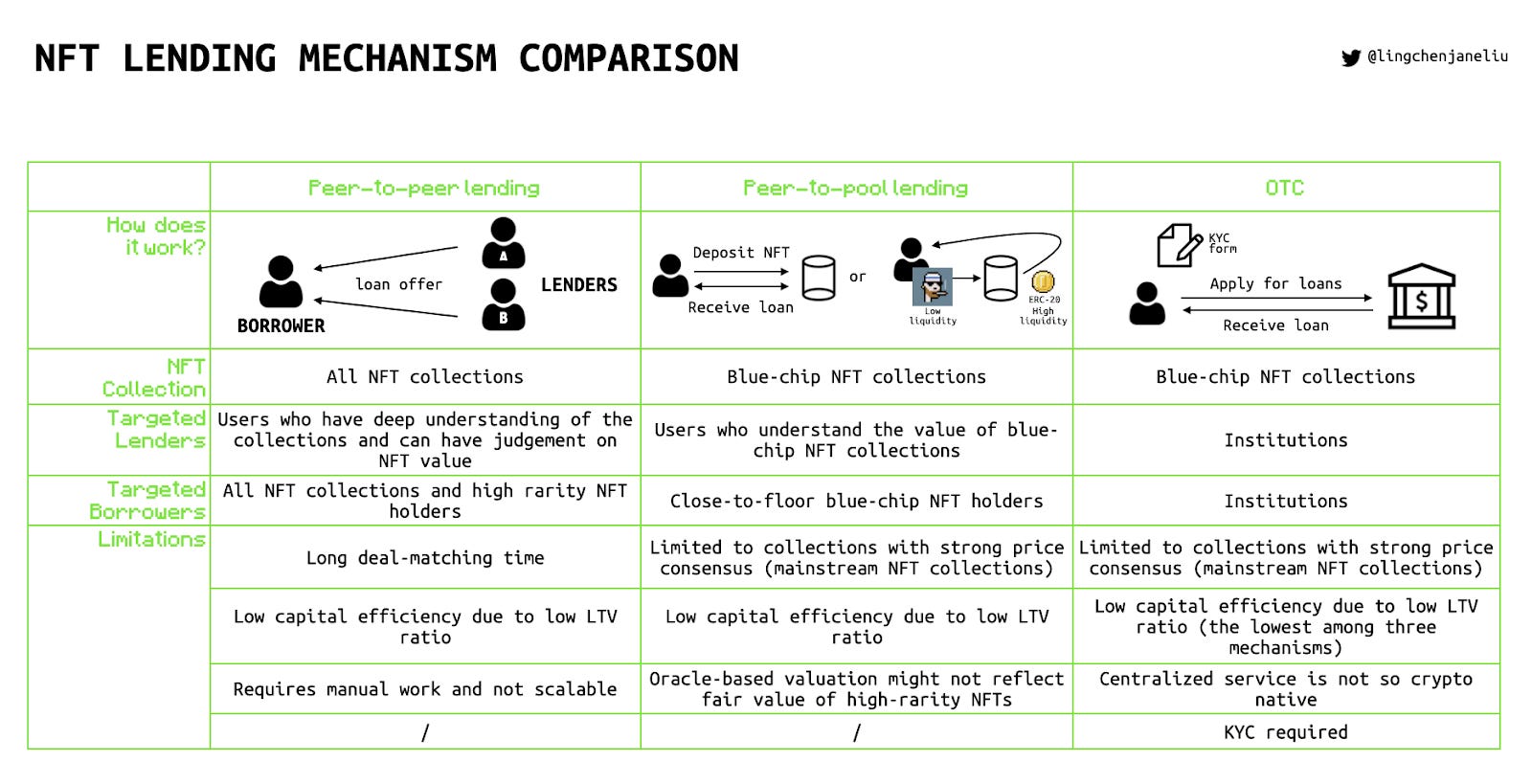

Peer-to-peer lending: In the P2P lending model, both parties need to judge and negotiate on the value of the NFT in order to reach consensus on loan terms.

Pros: The Peer-to-Peer lending mechanism leverages the classic escrow model and provides flexibility to allow coverage of a wide range of collections.

Cons: Since users need to negotiate each loan term with their respective counter-parties, loan fulfillment efficiency is low, which generally leads to higher APRs. It is also unlikely to have a high loan-to-value ratio as one single lender takes the entire loan risk.

Leading player: NFTfi

Peer-to-pool lending: The Peer-to-Pool lending model uses smart contracts to evaluate how much money a borrower can take out against their NFT collateral; the evaluation mechanism takes various factors into account such as the floor price of the NFT collection, trading volume, etc. When a borrower approves of the loan terms, they pledge their NFTs to the pool and get instant liquidity in return.

Pros: Peer-to-pool mechanism is a classic DeFi model. The process is simple and fast.

Cons: Peer-to-pool model works poorly for illiquid assets - like NFTs - due to low liquidation efficiency and low flexibility. The model doesn't work for non-floor determined collections (ENS, Artblocks) and for recently launched collections with insufficient historical transaction data. For high rarity/value NFTs, NFT holders can only manage to acquire loans with low loan-to-value ratio. Lenders might suffer from APR volatility as pool utilization changes.

Leading player: BendDAO

Over-the-counter (OTC) lending: Centralized NFT-backed loan provide.

Pros: Centralized solution is friendly for institutional players and can digest large volumes of NFTs at once.

Cons: Very low capital efficiency as centralized loan providers tend to offer a very low loan-to-value ratio to mitigate risk. Borrowers need to go through a know-your-customer process.

Leading player: Nexo

While most NFT lending projects fit into one of the three buckets I’ve mentioned above, I just recently came across an interesting project called Sodium, where they’ve been experimenting with an innovative loan fulfillment process via (what they call) “Hybrid Liquidity”.

SODIUM

Experimenting with a new NFT lending mechanism: Hybrid Liquidity

Sodium introduces a new lending mechanism,

Innovation on the Loan Fulfillment process

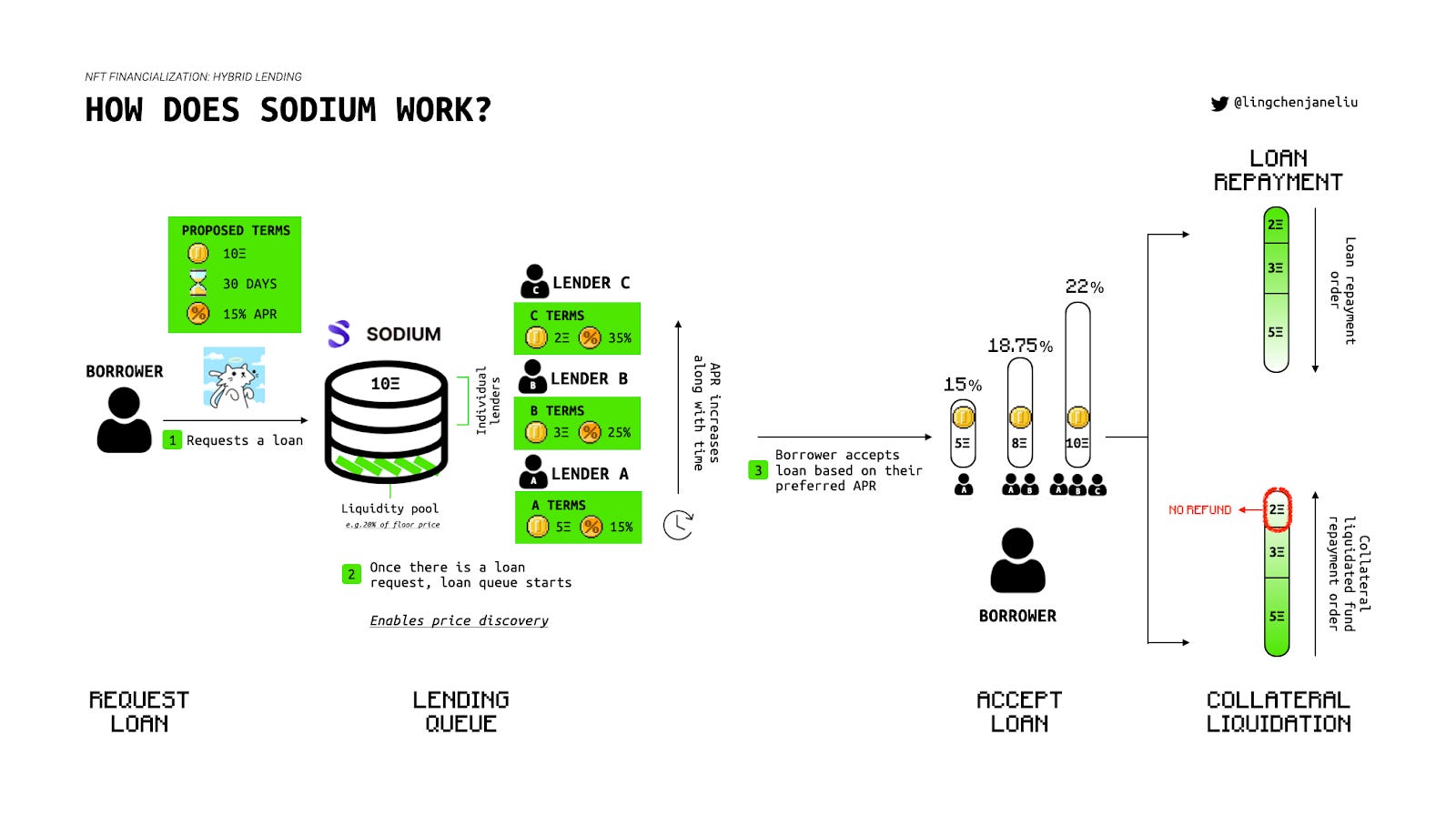

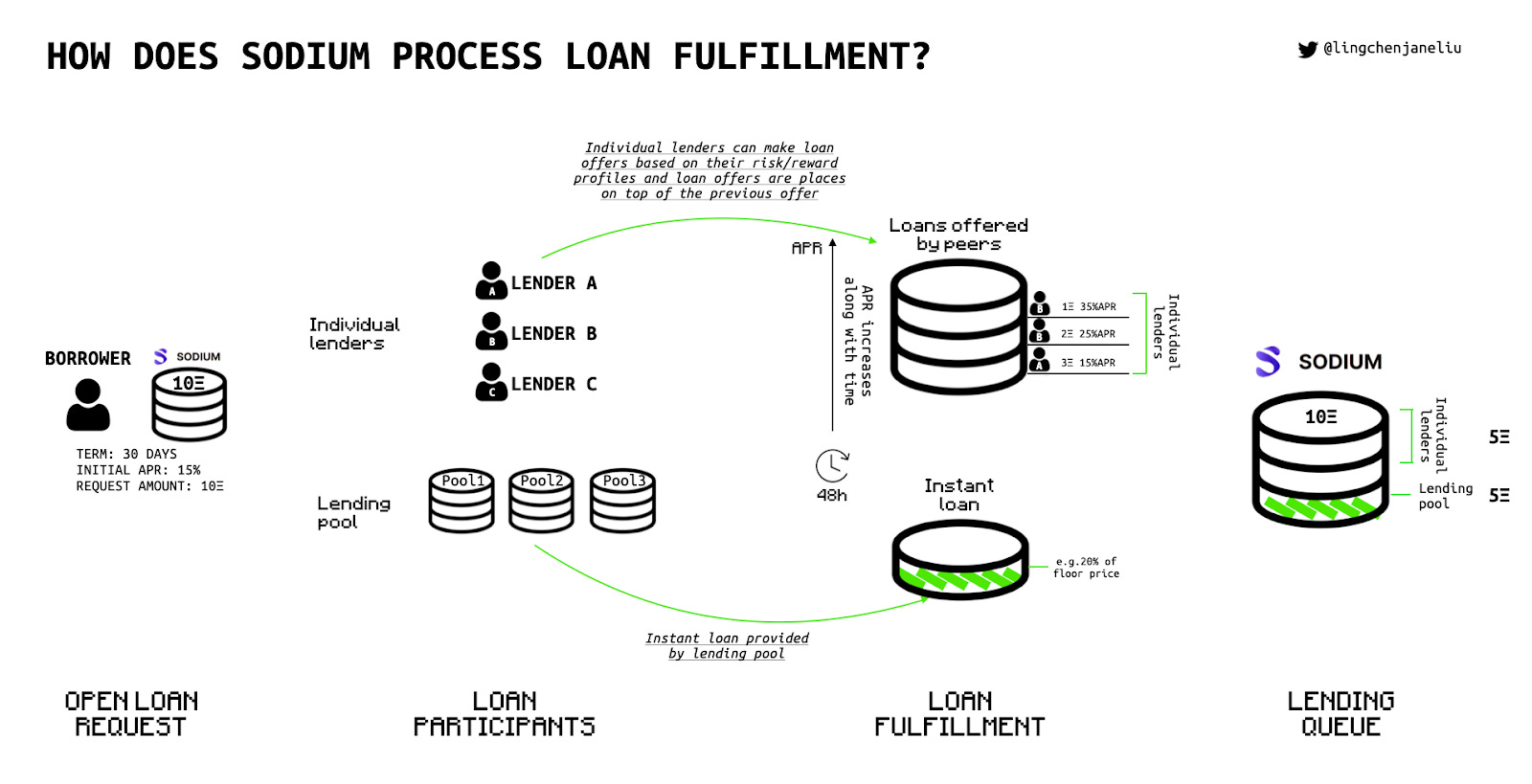

The borrowing process for Sodium feels similar to other NFT lending protocols in terms of user experience, yet there are some key differences on the loan fulfillment side, namely the price discovery mechanic of the loan request, and the lending queue, where borrowers choose how much hybrid (peer+pool) liquidity they want to accept.

Loan Request: After a borrower requests a loan, the loan request is open for 48h with hourly increasing APR, allowing efficient price discovery between lending and borrowing sides. Early lenders agree to a lower APR at lower risk, while lenders participating later are choosing higher reward for higher risk.

Lending Queue: Multiple lenders who provide ETH to a loan request are placed, in order, into the lending queue. Every offer provided by a lender is placed on top of previous offers; therefore, every lender participates at a different risk level. Different lenders provide liquidity based on their own understanding of the valuation of the collateralized NFT. Both peer and pool liquidity offers can be accepted via the lending queue.

Benefits of using the lending queue as a loan fulfillment process:

Instant loans: Borrowers acquire instant loans from pool liquidity

Flexibility: Lenders can participate with different risk tolerance

High LTV ratio: Users can leverage their NFT market knowledge to get high APR, while the borrower gets the maximum amount of liquidity the market is willing to provide

The lending queue mechanism, where APR increases for as long as the loan remains open, leads to better lending market price discovery. Each lender's loan contribution increases the collateral valuation by the amount of their contribution.

Sodium AMM combines pool and peer liquidity, enabling instant loans, high LTV and greater cost efficiency

Liquidity providers can create a lending pool for one or multiple collections or stake funds into any existing lending pools that meet their risk/reward profile. Pools can offer liquidity to loan requests according to a predetermined risk level as a percentage of the floor price, and take a place in the lending queue as any other lender. The fact that anyone is allowed to create a pool eventually will lead to higher competition for low risk positions resulting in better terms for borrowers.

Sodium AMM, by combining multiple pools and peers into the same loan request, enables instant loans, high LTV, and greater cost-efficiency, as higher APR is only for lenders who provide funds at higher valuation.

Liquidation mechanism

Collateralized NFTs are liquidated via liquidation auctions when the borrower fails to pay back the loan on time.

The first person to pay the "Buy It Now" price (which represents the total of all debts) immediately wins the auction.

If no one pays the "Buy It Now" price, the liquidation auction ends after 24 hours and the highest bid at the time when the auction ends is the winning bid.

If no bid was placed during the 24 hour liquidation auction period, the collateral will be transferred to the first lender in the lending queue, as the liquidity they provided acts as a bid by default.

Liquidation order:

Lenders get repaid from the bottom of the lending queue all the way to the top of the queue. That means that low-risk tolerance lenders get repaid first and high-risk tolerance lenders get repaid later.

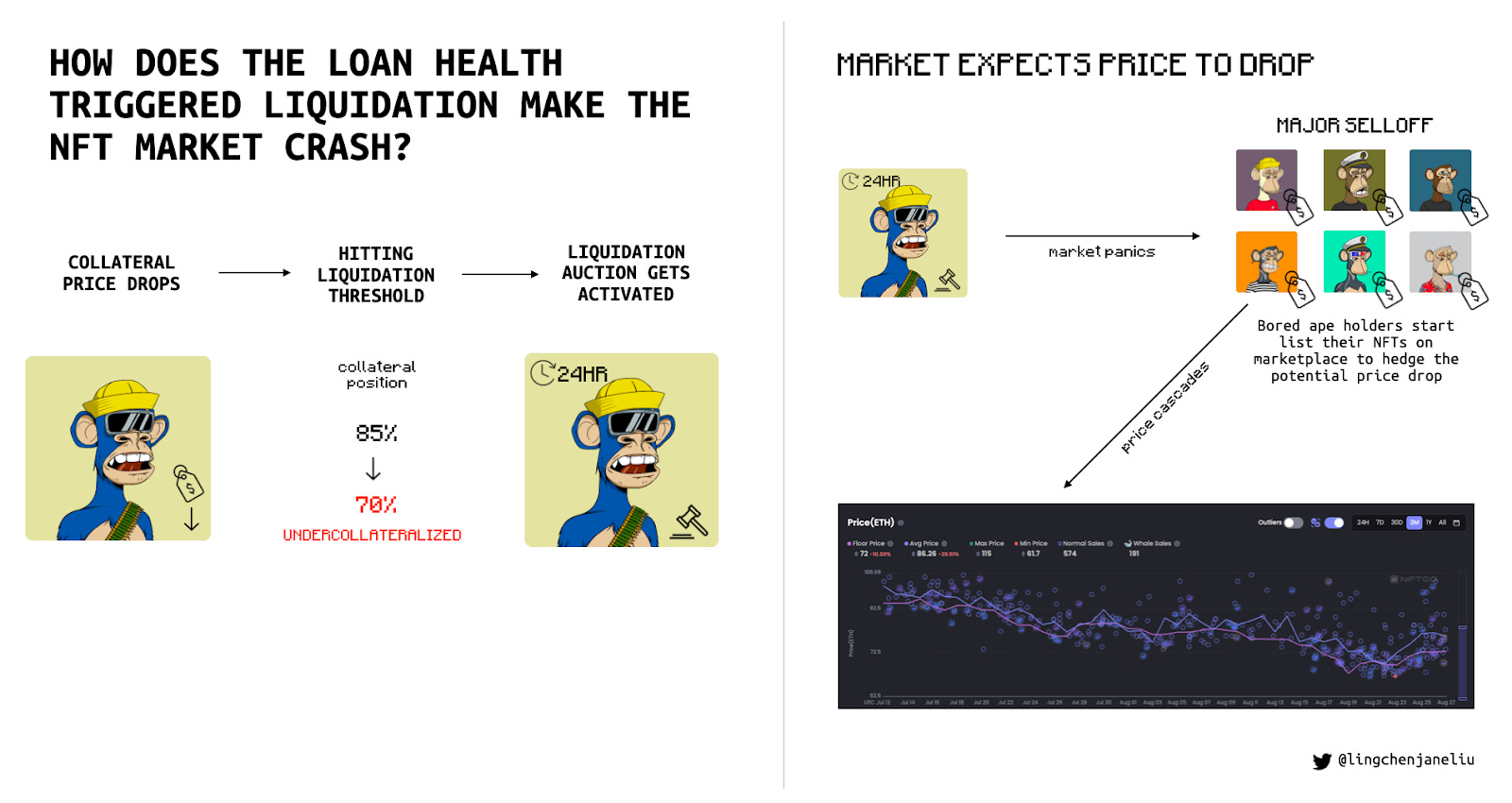

Time-triggered liquidation versus loan-health-triggered liquidation

The benefit of this time-triggered liquidation mechanism is that the lender commits to a specific collateral valuation for a specific time period upon contribution; if liquidation happens they can confirm commitment by paying the debts of lenders below them in the lending queue and then collect the collateral. At the same time, time-triggered liquidation will not start other loans’ liquidation processes and will not cause a liquidation cascade on the market. In contrast, the commonly adopted loan-health-triggered liquidation method used by P2Pool platforms such as BendDAO can easily trigger a large-scale selloff, which leads to a death spiral, like what happened during the recent liquidity crisis.

The NFT financialization market is still chugging along, even in the bear market, and builders are still building in the space. The market of course has its inherent issues - low liquidity and inadequate price discovery - and it is exciting to see new players in this space tackle those problems with innovative mechanism designs. During my research on Sodium, there were two things that really stood out to me, first being how the lending queue facilitates efficient price discovery, and second, how the hybrid liquidity mechanism aggregates liquidity to handle the low liquidity limitations. It’s still early days in the space, and it’s possible that we see an ‘ultimate solution’ emerge when NFTs as an asset class having more diverse utilities and use cases, but it is highly encouraging seeing the experimentation surrounding NFT-as-collateral.

I am excited to see what new trends develop in the NFT lending space and will be keeping my eyes on Sodium, not to mention being on the lookout for innovation in liquidation mechanisms, liquidity aggregation, and loan fulfillment, among others.

It seems like a new kind of ABS, different tranches have different risk-return profiles and within each tranch it is a AMM pool. How to divide the tranches properly?